Cost analysis and management

CMC is skilled and experienced at helping organisations get a better handle on cost management,

especially through the Activity Based Costing approach.

Activity-Based Costing (ABC) is an approach to managing costs that identifies activities in an organisation and assigns the cost of each activity to products and services according to the actual resources consumed by each activity. This contrasts with traditional cost allocation directly to cost objects.

The ABC method traces and allocates more of the indirect or overhead costs to specific items such as goods and services or even particular customer groups. This gives a clear X-ray of the way costs flow in the organisation and enables better decisions about resource allocation, and highlights areas for improvement, or customer segments that are potentially more or less profitable.

ABC enables the mapping of cause and effect relationships to more accurately assign costs. Once costs of the various business processes have been clarified, the cost of each activity is attributed to each product to the extent that the product uses the activity. In this way ABC often identifies areas of high overhead costs per unit and so directs attention to finding ways to reduce the costs or to charge more for costly products. For example, increased application of IT and integrated manufacturing has drastically reduced direct labour costs in many firms, and has increased depreciation, which is an indirect cost.

Like manufacturing industries, service industries have a range of products and customers, which can cause cross-product, cross-customer subsidies. Activity-based costing enables the teasing out of these potential subsidies so that more rational decisions can be taken about how various products and customer segments.

especially through the Activity Based Costing approach.

Activity-Based Costing (ABC) is an approach to managing costs that identifies activities in an organisation and assigns the cost of each activity to products and services according to the actual resources consumed by each activity. This contrasts with traditional cost allocation directly to cost objects.

- In traditional cost accounting it is assumed that cost objects consume resources whereas in ABC it is assumed that cost objects consume activities.

- Traditional cost accounting mostly utilises volume related allocation bases while ABC uses drivers at various levels.

- Traditional cost accounting is budget accountability structure-oriented whereas ABC is business process-and output oriented.

The ABC method traces and allocates more of the indirect or overhead costs to specific items such as goods and services or even particular customer groups. This gives a clear X-ray of the way costs flow in the organisation and enables better decisions about resource allocation, and highlights areas for improvement, or customer segments that are potentially more or less profitable.

ABC enables the mapping of cause and effect relationships to more accurately assign costs. Once costs of the various business processes have been clarified, the cost of each activity is attributed to each product to the extent that the product uses the activity. In this way ABC often identifies areas of high overhead costs per unit and so directs attention to finding ways to reduce the costs or to charge more for costly products. For example, increased application of IT and integrated manufacturing has drastically reduced direct labour costs in many firms, and has increased depreciation, which is an indirect cost.

Like manufacturing industries, service industries have a range of products and customers, which can cause cross-product, cross-customer subsidies. Activity-based costing enables the teasing out of these potential subsidies so that more rational decisions can be taken about how various products and customer segments.

|

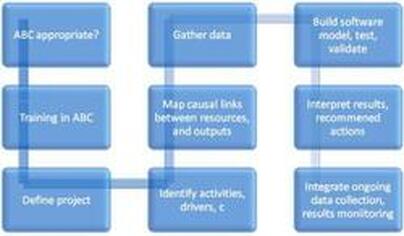

Activity-Based Costing Project- typical steps

|

Activity-Based Costing Project- typical benefits

CMC has used ABC methods in various settings to

|

CMC is experienced and equipped to help you through all stages of such a project. We are skilled at adapting the method to different organisations, in both commercial and public sectors. We avoid the excessive complexity of software models used in other approaches. CMC is experienced at keeping the data collection load to requisite and manageable levels to suit the size and nature of the organisation.